2025 went by in the blink of an eye. Wall Street predictions were downbeat back in January, while European equities were also downplayed at the start of the year. Despite this, and a year packed with potential upsets, equity markets provided yet another year of double-digit returns.

Bonds achieved a perfectly respectable return over the year, and inflation globally saw a slow but steady progression downwards, helping central banks cut rates several times across the year.

The UK ended 2025 with inflation at roughly 3.2% in the year to November, having fallen from 3.9% in January. While inflation still sits above target levels globally, given the implications of US tariffs and the Budget closer to home, the year showed solid progress in the battle against sticky inflation.

Keep reading for your economic review of the year.

The power of bond markets

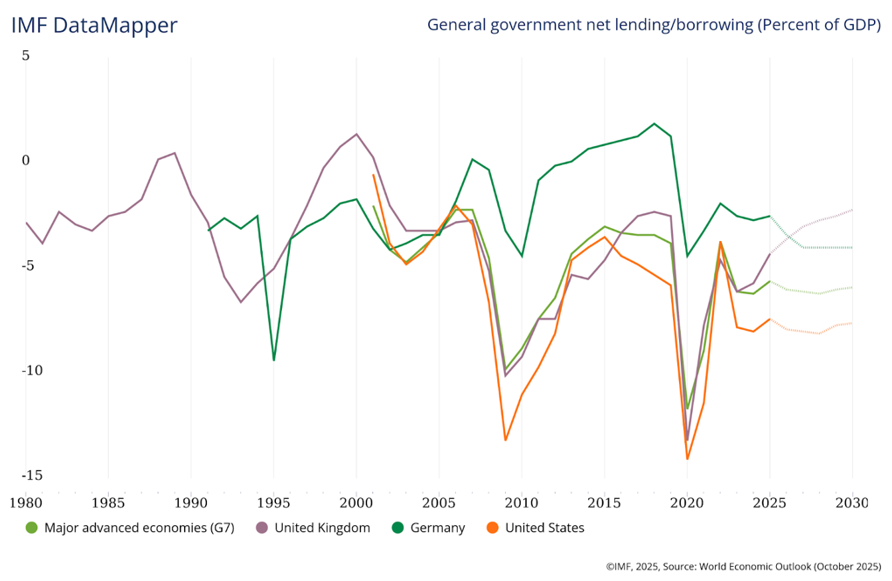

While equity markets have continued to capture global attention with another year of high growth, debt markets have quietly been influencing the global economy in a significant way over the past year. At the end of 2025, global government debt stands at over $100 trillion according to the International Monetary Fund (IMF), exceeding 235% of global GDP. Government debt in the developed world has been a particularly important topic in 2025, with bond investors expressing growing concerns that governments are not doing enough to curtail uncomfortably high debt levels.

The chart below illustrates how government net borrowing as a percentage of GDP has evolved. Values below zero indicate budget deficits, so deeper dips on the chart reflect heavier government borrowing. The sharp drops during major crises, particularly COVID, show how fiscal balances deteriorate in periods of stress. While borrowing has improved since then, it remains elevated compared to earlier periods, with implications for debt levels and bond yields.

Source: World Economic Outlook (October 2025)

The UK, in particular, has been subject to global scrutiny over the past year, with debt markets viewing Labour’s fiscal plans unfavourably and expressing uncertainty about Britain’s ability to control its finances. The government’s debt burden is large relative to the size of the economy, and public finances could face strain over time. While these levels are elevated, they are not the highest the UK has experienced, suggesting that the challenge is one of sustainability and credibility rather than an unprecedented fiscal position.

This was the backdrop for the Budget in November, leaving Chancellor Reeves in a difficult position, with little leeway to fund spending. Gilt markets appeared to reflect this, with investors selling long-dated gilts and thereby increasing yields. Those who remember the mini-Budget crisis of 2022 may recall that sharp moves in gilt yields can be a sign of reduced investor confidence, and that this dynamic contributed to Bank of England intervention to maintain financial stability.

When push came to shove, Reeves delivered a Budget that was received more positively by debt investors, with some commentators suggesting it was designed to reassure gilt markets. With increases in tax revenues and extensions to the income tax band freezes, bond investors viewed this as the government taking a step towards curbing borrowing. Gilt yields fell, and with them the cost of government borrowing. This is a sign that bond market “vigilantism” may be here to stay, and that investors may have a reduced tolerance for high deficits without credible fiscal plans.

Source: House of Commons Library, Public finances: Economic indicators 2025

Despite the UK’s position, we are not experiencing a debt crisis at present. A crisis can be difficult to define and depends on several complex factors, which means that levels of debt can vary widely between countries before there are major default concerns. Japan is a notable example of these differences in practice. Japan currently sits on an extremely high level of government debt for a country in peacetime.

There are several reasons for this. First, Japan has had much lower interest rates than other countries. Second, its debt profile differs from many other developed economies. Monetary policy in Japan has also differed from the rest of the world: after a prolonged period of negative interest rates, it has only recently moved back into positive territory. This has helped suppress yields in recent years.

There is potential for this to change in the coming years as Japan faces pressure to tackle inflation through higher interest rates, while also aiming to keep debt-servicing costs down. Japan is also unique in that the majority of its debt is held domestically; in fact, the Bank of Japan holds almost half of the government bonds in issue. Unlike debt held by international investors and institutions, this can, in practice, mean that debt can be rolled over for longer periods. This is not to suggest that Japan’s debt position is risk-free; rather, it serves as an example of how complex debt dynamics and public finances can be across countries.

So, 2026 will likely be another interesting year for bond markets. The US Federal Reserve Chair, Jerome Powell, is due to finish his tenure in May. While this would not normally be expected to cause significant market concern, he has been a long-time adversary of Trump, who previously raised the prospect of removing him early in his second term. At the time of writing, Trump is interviewing potential replacements. There has been speculation over whether he will choose a successor perceived to be more politically aligned.

This may matter because central banks typically aim to operate independently from the government. Independence can help avoid monetary policy being driven by short-term political objectives, which can have implications for inflation and economic growth over the longer term. The Fed often acts as a catalyst for global interest rate trends, so this may encourage investors to remain cautious going into 2026.

Valuations: Boom or bust for US exceptionalism?

There seems to be a buzzing narrative surrounding the markets this year that has thoroughly taken root in the minds of investors. US equities have been going from strength to strength with expectation-defying returns, with the S&P 500 delivering double-digit returns (for US $ investors) for the third consecutive year. However, there’s a lingering concern that these returns are unsustainable and that valuations may be too expensive given the underlying company fundamentals. This stems from multiple sources, including Schroders‘ data indicating that current US valuations, as measured by CAPE, are near their highest levels in over 140 years. While Timeline, or anyone else for that matter, may not be able to provide a definitive answer as to whether valuations will take a hit over the next year, it is worth considering some key points. Firstly, a high valuation does not necessarily mean an asset is overvalued.

It’s worth thinking about two of the major components that drive index returns: earnings growth and monetary policy. Let’s consider the earnings growth of companies in the S&P 500. As of the time of writing, 91% of companies in the index have reported their earnings for the year, according to Forbes, and of that 91%, 82% have beaten consensus earnings estimates. This is impressive profit growth and presents a different perspective from previous financial shocks, such as the 2000s dot-com bubble, where many companies failed to reach profitability. While no one can truly predict what may happen to future earnings, analysts do believe that profit growth may continue in the US. JP Morgan reports that it expects 13% to 15% annual earnings growth over the next two years, driven by both the heavy-hitting Magnificent 7 and the broader market (as reported by Reuters). The broadening of this market is a positive sign for those concerned about the particularly high valuations of the Magnificent 7, which are being fuelled by AI.

While earnings growth is important for valuations, monetary policy also plays a role. In the US and across developed markets more generally, interest rates have been reduced from the post-COVID highs that were used to curb inflation, which we can see in the effective Fed rate graph below. The Fed may have been cautious with its cuts in 2025, but compared to historical averages, the US is currently on the lower end of the rate spectrum. When interest rates are low, this can impact bond returns, making them less attractive than equities for some investors. This can cause equity prices to rise as investors search for higher returns. Given relatively low interest rates alongside strong earnings growth, these factors can help explain the current high valuations in the US.

Source: Federal Reserve Bank of New York (2025)

However, stocks don’t exist in a vacuum. For the US to be considered overvalued, investors are likely comparing it with alternative options for their capital. It follows that other international markets may be more attractively valued or potentially undervalued in comparison. European stocks have emerged as the obvious alternative this year, particularly given their strong market performance relative to those in the US.

At the time of writing, price-to-earnings (P/E) ratios for both the US and Europe do not fully reflect the discrete market performances of the two regions. There is currently a wide valuation gap, with the US trading on a P/E multiple of around 28x compared to roughly 18x in Europe. This implies that US equities are valued at roughly 55% higher than European equities. For valuations to converge, Europe would need to see an increase of around 55% in prices, assuming no change in earnings, or a roughly 36% decline in US equity prices if earnings were unchanged. Valuations could also converge if the US were to experience a roughly 55% increase in earnings, all else equal.

If you compare US valuations to emerging markets (EM), the disparity is even wider, with the US trading on a P/E multiple around 1.7 times higher than EM, which currently sits at roughly 16.3x. It is important to stress that a lower P/E multiple does not automatically signal an attractive investment. Valuations need context. Some markets are cheap for good reasons, reflecting structural, political, or governance risks, rather than overlooked opportunities.

As a final note on valuations, it is important to consider that we are moving into uncharted territory. Concerns are particularly heightened around AI and the impact this technology may have as we move forward. It is becoming increasingly rare to find an individual or a company that hasn’t embraced the technology to streamline workflows. Even with widespread adoption, markets are still finding it difficult to price a technology that is advancing at an exponential pace, without a clear view of what it can ultimately achieve.

Technology stocks have been driving these high US valuations, with the sector rising roughly 22% over 2025 in the S&P 500, according to US Bank. This has fostered a sense of vulnerability in the markets to potential missteps, contributing to investor nervousness. However, there is also a case that this represents a structural change, not just in markets but a broader societal transition as adoption accelerates. There will undoubtedly be winners and losers, and at the moment, it is unclear who these may eventually be. Diversification remains an important tool for investors to prepare for both the successes and setbacks that may come from this transitional period.

The question then becomes: what does this renewed focus on valuations actually mean for investors? At its core, it should serve as a reminder to keep a long-term perspective. Short-term noise can make markets feel overvalued and tempt investors to plan around an imminent correction, but history shows that this is a difficult and often unrewarding game. Successfully stepping out of markets and then re-entering at the right time requires getting it right twice, which is difficult to do consistently.

Over the long run, global equity markets have continued to grow despite periodic corrections. While this journey inevitably involves short-term volatility, evidence supports staying invested as a more reliable path to long-term growth. Against this backdrop, valuation differences reinforce the importance of global diversification. A global market-capitalisation approach remains an efficient and highly diversified way to allocate capital, reflecting where markets collectively see the strongest opportunities today.

Touching on tariffs

It feels almost criminal not to address the buzzword of 2025 in our end-of-year review. (Ironically, there is now a question over whether the tariffs themselves may be unlawful, pending a US Supreme Court ruling.) US tariffs were monumental in shifting geopolitical relationships. With the effective US tariff rate now settling at around 18%, the highest level since 1934, it is likely that international relations and geopolitical tension will continue to be a key theme into 2026.

The initial positive news is that there has been some stabilisation since the tariffs were introduced, with the US striking trade deals with regions such as the UK, the EU, and Japan. However, relations were less smooth with the world’s second-largest economy, China. After the tense exchange of escalating tariffs following “Liberation Day”, relations appeared to calm somewhat. There is currently a “tariff truce” between the two nations, but there is potential for tensions to escalate as we move into next year. One of the biggest global impacts has been the shift in supply chains.

Perhaps it might be hard to believe with such a backdrop, but China has shown resilience throughout 2025. In November, CNN reported that it became the first country to reach a record trade surplus of $1 trillion. While this is positive for China, it may prove a thorn in Trump’s side, as China may be able to take a firmer approach in future negotiations. Some reporting suggests a key driver behind this surplus has been China’s ability to diversify away from the US, towards regions such as Europe, Africa, and Southeast Asia.

Potential tariff impacts may emerge in 2026, depending on the Supreme Court’s decision on whether the tariffs are lawful or unlawful. Should the tariffs be deemed unlawful, US stocks could benefit. Companies took a hit in 2025, having absorbed some of the tariff costs; with tariffs reduced, any short-term relief may help support corporate earnings. An additional boost could come in the form of government refunds from these tariffs, which CBS suggests may be as much as $168bn owed to businesses.

Regardless of the outcome, Trump’s tariffs have impacted markets this year and may continue to do so in the years ahead. The shift in global trade dynamics is still developing, and there remain a number of trade deals left to be signed between nations. In periods of uncertainty, volatility can increase over the short term. Investors taking a well-diversified approach are likely to be best placed to navigate what comes next.

Asset class review

2025 has been a year of resilience for markets. The year started with concerns about a new trade war and policy shocks from the US, but markets held up better than many expected. Instead, it became a year of adjustment: inflation stayed sticky, trade policy tightened in a more measured way than feared, and a spring drawdown in equities was followed by a broad-based recovery, with major indices reaching new highs by year-end. Bonds were steadier than in recent years, with higher starting yields providing a useful income cushion and helping to dampen portfolio volatility as rate expectations gradually shifted towards cautious cuts.

Proxies: Asia ex-Japanese Equities: Morningstar Asia Pacific ex-Japan Large-Mid Cap GR GBP; Developed Market Equities: Developed Market Equities: Morningstar Developed Markets Target Market Exposure GR GBP; Emerging Market Equities: Emerging Market Equities: Morningstar Emerging Markets Target Market Exposure GR GBP; Europe ex-UK Equities: Europe ex UK Equities: Morningstar Developed Europe Target Market Exposure GR GBP; Global Bonds: Global Bonds: Vanguard Global Bond Index Hedged Acc GBP in GB; Global Corporate Bonds (hedged £): Vanguard Global Bond Index Hedged Acc GBP in GB: Global Equities: Global Equities: Morningstar Global Markets GR GBP; Global Growth Equities: Global Growth Equities: Morningstar Global Growth Target Market Exposure GR GBP; Global Property: Global Property: Morningstar Global Real Estate GR GBP; Global Value Equities: Global Value Equities: Morningstar Global Value Target Market Exposure GR GBP; Japanese Bonds: Japanese Bonds: Morningstar Japan Treasury Bond TR GBP Hedged; Japanese Equities: Japanese Equities: Morningstar Japan GR GBP; Overseas Government Bonds: Overseas Government Bonds: iShares Overseas Government Bond Index (UK) D Acc in GB; UK Equities: UK Equities: Morningstar UK GR GBP; UK Government Bonds: Vanguard UK Government Bond Index Acc GBP in GB; US Equities: US Equities: Morningstar US Target Market Exposure TR GBP. Performance periods: 4th Quarter: 30/09/2025 – 31/12/2025, Year: 31/12/2024 – 31/12/2025; 3 Year: 31/12/2022 – 31/12/2025, 5 Year: 31/12/2020 – 31/12/2025.

Equity: Diversified momentum

Global equities delivered strong returns in 2025 despite tariff uncertainty, shifting central bank expectations. and a sharp bout of volatility in April. The key theme was a broadening of market leadership. The year began with gains concentrated in a small group of US mega-cap technology companies, but by the second half, the rally had become more global and more diversified. AI remained an important driver of sentiment, yet the “Magnificent Seven” were no longer the sole engine of index-level returns according to MarketWatch.

Source: Timeline (31.12.24 to 31.12.25). Returns shown in GBP

US equities delivered another year of positive returns, although performance lagged the strongest international markets. US equities returned around 9.63% in 2025, reflecting steady but more moderate progress than in the previous two years. In the first half, gains were heavily influenced by AI-linked businesses within the “Magnificent Seven”, as investors continued to price strong demand for cloud computing, data centres, and semiconductor capacity. As the Federal Reserve began to cut rates in the autumn, leadership broadened: small caps rallied as borrowing costs fell, financials and healthcare benefited from improved earnings visibility, and industrials strengthened alongside firmer demand.

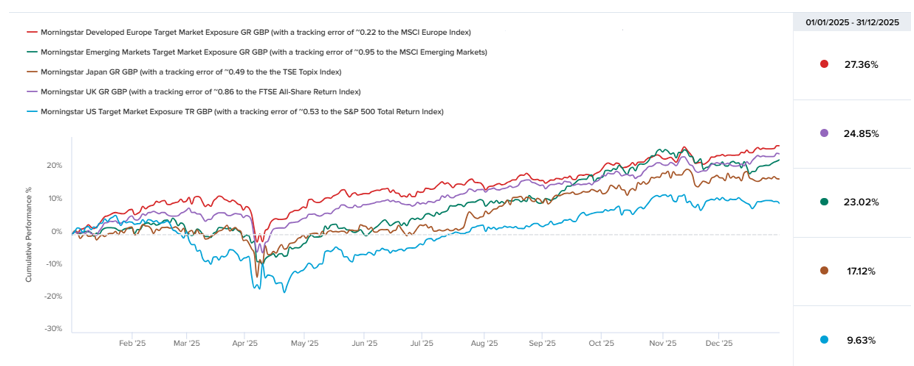

UK equities made a stable contribution to global portfolios, returning 24.85% over the year. Large-cap performance was supported by the FTSE 100’s exposure to energy, mining, and globally diversified firms, which benefited from stabilising commodity markets and stronger external earnings. Mid-cap shares saw improved sentiment as inflation pressures eased and the Bank of England adopted a more accommodative tone. While the UK lagged the strongest-performing regions, it delivered steady returns. As we discussed in our Economic Outlook, UK valuations remain attractive relative to other global regions.

Source: Timeline (01.01.25 to 31.12.25). Returns shown in GBP.

European equities also delivered strong results, returning 27.36% in 2025. Industrials and capital goods companies benefited from improved export conditions and higher spending on automation, semiconductor equipment, and AI-related infrastructure. Electrification and defence also benefited from large EU programmes such as the €800 billion NextGenerationEU plan, alongside broader rearmament initiatives. Financials and utilities also contributed as inflation eased and governments maintained higher investment in the energy transition and defence. Although parts of manufacturing, particularly in Germany, remained under pressure, European equities were supported by relatively attractive valuations and a broad mix of sector winners, rather than dependence on a small group of technology giants.

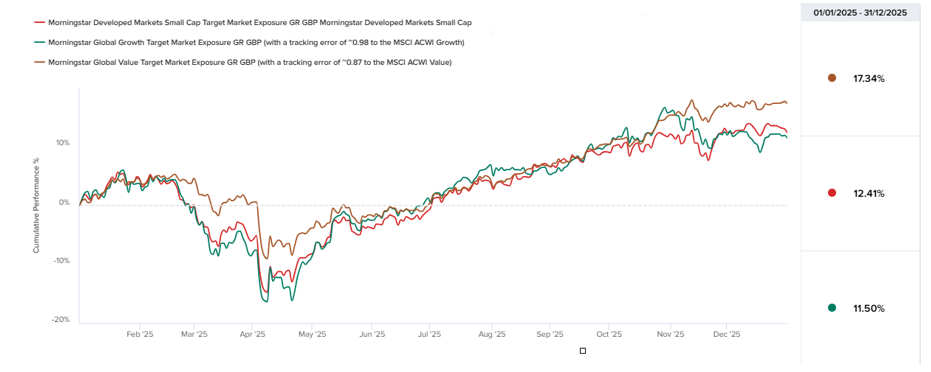

Emerging Markets (EM) were another major contributor to global equity returns. Technology supply chain markets such as Taiwan and South Korea benefited in particular, with semiconductor and memory stocks (companies involved in the manufacturing of memory chips) among the strongest performers. Later in the year, some profit-taking added volatility. Latin American markets, such as Brazil, improved as inflation trends moderated and commodity prices stabilised. China was mixed, with periods of policy support lifting sentiment but structural challenges limiting momentum. Overall, Emerging Markets delivered some of the strongest regional returns of the year, with AI and technology supply chains a key part of the story.

Japan remained one of the stronger developed markets. Ongoing corporate governance reforms, rising share buybacks, and improved capital discipline supported returns. Japanese equities continued to trade at a valuation discount to the US, which helped sustain international interest.

Source: Timeline (01.01.25 to 31.12.25). Returns shown in GBP.

From a factor perspective, growth and AI-linked stocks still performed well, but they were no longer the only driver of global equity returns. As inflation eased later in the year and markets became more confident that interest rates had peaked, performance broadened into more cyclical and value-oriented areas. Sectors such as financials, industrials, and energy contributed more to returns, particularly in Europe, where these sectors account for a larger share of the index. Early in the year, large-cap growth, particularly US mega-caps, led the rally. Later, as recession fears faded and policy expectations shifted lower, small, and mid-caps improved and closed some of the gap. This is consistent with past periods where easier monetary policy has supported more economically sensitive companies.

Taken together, 2025 marked a shift from narrow, AI-led performance dominated by a small group of US mega-caps to a more balanced and diversified equity environment. Market leadership broadened across regions and sectors as the year progressed, supported by resilient earnings and improving investor confidence. From a factor standpoint, returns shifted away from being mainly driven by large-cap growth stocks, as value stocks, emerging markets, and smaller companies had a greater influence later in the year. For long-term investors, this reinforced the value of global diversification and staying invested through periods of volatility, with AI demand increasingly supporting a wider range of companies rather than a handful of headline names.

Fixed income: Stability amid easing and elevated yields

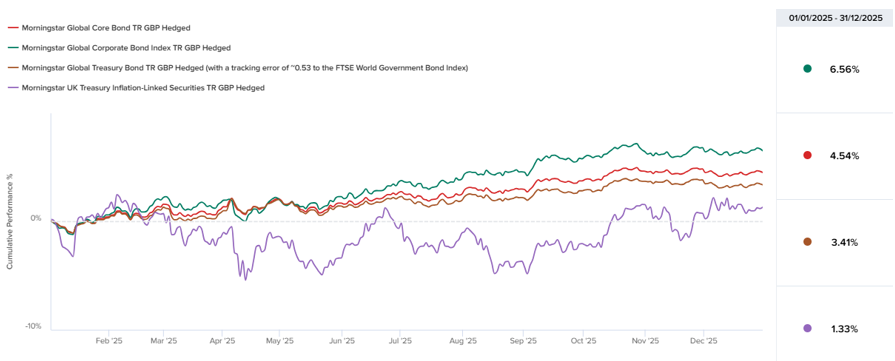

Fixed income was more stable in 2025. Yields remained higher than before the pandemic, coupon income was a meaningful driver of total returns, and bonds again helped diversify portfolios during periods of equity market volatility. This was reflected in index performance, with global corporate bonds leading, core bonds and Treasuries delivering more modest gains, and UK inflation-linked gilts lagging over the year.

Source: Timeline (01.01.25 to 31.12.25). Returns shown in GBP

US bonds were mainly driven by the shift in Fed policy. As markets moved from “higher for longer” towards rate cuts, short-dated yields fell, but longer-dated Treasuries were more volatile. Concerns about government borrowing and heavy issuance kept pressure on the long end, which is consistent with government bond returns being more modest than credit over the period.

UK government bonds had a tougher spell at times during the year, with yields rising as investors reacted to political uncertainty and fiscal headlines. The run-up to the autumn Budget was a clear pressure point for gilts, as markets focused on fiscal credibility, the scale of borrowing, and the risk of tougher tax and spending choices. The most significant moves were in long-dated gilts, particularly 30-year maturities, while short-dated gilts were steadier and largely followed Bank of England rate expectations.

The tone improved later as the Budget was viewed as more credible and expected gilt supply appeared lower than feared, with the Institute for Public Policy Research (IPPR) noting early signs that the UK’s borrowing cost premium relative to peers may be starting to unwind. UK index-linked gilts underperformed as rising real yields and their very long duration weighed on prices. Inflation expectations stabilised rather than increased, limiting the benefit of inflation protection, while heavy government issuance and episodes of fiscal volatility added further pressure, particularly at the long end of the curve.

Eurozone government bonds were relatively steady as the European Central Bank moved rates lower and then paused, anchoring the front end even though longer maturities continued to move with global rates and supply. ECB analysis also noted that rising defence spending plans are among the factors investors are watching when pricing longer-dated euro area government bonds. EFAMA data pointed to continued investor demand for bond funds and ETFs throughout the year, supporting the broader fixed income backdrop. Emerging market debt was one of the brighter areas, especially local currency exposure, supported by high yields and improving sentiment. In parts of Latin America, stronger currencies also helped returns.

Overall, 2025 reinforced a simple message for fixed income: earning interest matters again. Better outcomes came from combining diversified aggregate exposure with corporate credit, while keeping a close eye on duration risk, particularly in long-dated government bonds where fiscal supply concerns persist.

Glittering gold and crypto casualties in 2025

Each quarter, we include a short spotlight on a theme beyond the core asset classes to provide broader market context. This quarter, we focus on gold and cryptoassets, which have attracted renewed investor attention and are often discussed as potential alternatives or hedges during periods of market uncertainty.

In 2025, alternatives were back in the spotlight. Gold and cryptoassets were both discussed as potential diversifiers and, at times, as possible “safe havens”. The year’s price action made the differences clearer. Gold delivered a very strong annual gain. Bitcoin also had a strong run earlier in the year, reaching a record high in October, but then sold off sharply, including a fall of around 36% from its October peak. By late November, it had given up its year-to-date gains.

Gold’s strong 2025 performance was supported by heightened economic and geopolitical uncertainty, shifting interest rate expectations, and strong investor and central bank demand. Evidence also suggests these drivers may have a more structural element in this cycle, with central bank and investor demand expected to remain supportive into 2026. However, gold remains a non-yielding asset, so returns derive primarily from price movements, and it can remain volatile, particularly when real yields rise or the US dollar strengthens. Academic research also adds a note of caution, suggesting that gold’s safe haven behaviour has weakened over time and that it can sometimes move more in line with equities during periods of market stress (Faraj, H. et al., 2025).

Cryptoassets told a different story. Bitcoin’s drawdown from its October high and the broader market weakness were consistent with how crypto has typically behaved in risk-off phases. As investors became more cautious and risk appetite faded, crypto traded more like a high-risk asset than a defensive one. This underscores why crypto remains a speculative asset class, driven mainly by sentiment, liquidity conditions, and positioning, rather than fundamentals such as cash flow. This pattern also reinforces a broader point: when liquidity tightens and risk appetite falls, cryptoassets have historically been vulnerable to sharp drawdowns. Even after strong rallies, moves can reverse quickly, which limits their reliability as a defensive holding.

Source: Timeline (2025)

The Timeline chart above helps put gold’s role in context. It shows that different assets lead at different times, and that gold can have strong periods but also meaningful swings. It is best viewed as a supporting diversifier, rather than a guaranteed stabiliser.

So, can gold and Bitcoin be considered safe havens? Gold can sometimes behave defensively and can help diversify portfolios over time, but 2025 also showed it is not a guaranteed stabiliser, especially after a strong rally. Cryptoassets are not reliable safe havens. Their large drawdowns during shifts in risk sentiment limit their usefulness as a protective measure in stressed markets.

From a portfolio perspective, 2025 was a reminder that relying on any single alternative asset for protection is challenging. A well-diversified mix of global equities and high-quality bonds has typically been a more consistent way to manage risk over time. Equities remain the main source of long-term growth, while high-quality bonds can help cushion portfolios when equity markets are unsettled. Gold can sometimes help as an additional diversifier, but it is best viewed as a supporting holding rather than the foundation of a long-term portfolio.

Reflections on the year

We must confess, each year when we come to write these reviews, there is a fear that we sound a little like a broken record. The pattern emerges that markets continuously evade their predicted path and throw a spanner or two into the works for good measure. 2025 was really no different. Despite the meandering path, markets continued to deliver a fantastic return for investors, highlighting once again that keeping calm and staying invested has historically been a strong course of action.

From our perspective, some key themes that emerged last year will likely transition into 2026 and form prominent drivers for markets as a result. Geopolitical tensions have been a strong undercurrent over the past couple of years, and 2026 may be no different. There is still ongoing conflict between Russia and Ukraine, and a precarious peace in Israel and Palestine, leading to concerns about long-term stability in the region. The US also released its National Security Strategy document in December, which sent a few shockwaves through Europe and may influence the outlook over the next year.

AI is at the forefront of everyone’s minds at the moment, with many believing that we may be on the verge of a structural shift in society. Concerns surrounding artificial general intelligence, commonly referred to as AGI, are central and arise from both sides of the debate: firstly, whether it would ever be possible to truly create artificial general intelligence, and secondly, whether this is something that we as a species want to pursue at all. Progress in quantum computing also continues in leaps and bounds, driving forward the potential for discoveries and breakthroughs. Whether or not all of the lofty hopes for AI and computing are achieved, it is clear that these technologies are going to remain an important theme as we move forward.

Despite what the next year throws our way, we remind our readers to consider the evidence and historical data before reacting. Volatility is part and parcel of investing and is simply the price of admission for long-term returns in the markets. It is key that we don’t let short-term movements drive investor behaviour. Having faith in well-structured and robust financial plans, alongside investing in well-diversified and well-crafted investment strategies, is an important part of navigating what the next year might bring.

As a final sign-off from the whole team at Timeline, we would like to say thank you to each reader who has supported us for another fantastic year. We truly wouldn’t be where we are today without the support and trust of advisers like yourselves. At Timeline, we want to help as many people as possible to plan, invest, and retire with confidence and support them on their way towards greater financial freedom. We understand the level of trust this requires from yourselves and your clients, and we are fully committed to supporting you on this journey.

May 2026 be the best year yet, filled with success, happiness, and growth.

Production

Production