2024 was one for the history books. The “Barbenheimer” debate was finally put to bed at the Oscars, Taylor Swift’s Eras tour made her the first billionaire artist from songs and concerts alone, and the Paris Olympics and Paralympics provided a sporting spectacle that left viewers speechless.

We were all kept on our toes when it came to politics too. In the UK, we welcomed Mr Starmer into Number 10 with an overwhelming majority. Yet, his premiership has been fraught with challenges, not least Rachel Reeves’ “painful” budget. The consensus was that “it could have been worse”, but changes to Capital Gains Tax (CGT), Business Property Relief, and Inheritance Tax (IHT) have already proven to be a headache. The freezing of various tax rate bands, meanwhile, continues the tradition of fiscal drag for the average household.

Businesses were also hit hard. The combination of an increase in employer National Insurance to 15% and a reduction in the Employment and Support Allowance threshold presents an expensive challenge that could dampen business confidence going forward.

Economic outlook and market commentary

We start 2025 with Trump once again headed to the White House, and with that comes a sense of great trepidation around the globe. His decisive victory left many political pundits and exit polls in shock, but the markets breathed a collective sigh of relief.

The effects of this result won’t just be felt in the US. Trump’s foreign policies are somewhat aggressive. Under his first presidency, and according to the Tax Foundation, his tariffs resulted in Americans paying an additional $80 billion in taxes. These tariffs have already shifted the international import market, with China now falling behind Mexico in terms of its share of US imports.

Trump’s campaign pledge included a 10% flat-rate tariff on all imported goods, excluding Chinese goods, which would face a steeper 60% tariff, and Chinese car imports, which could face a potential 100% tariff. The risk here is rising inflation. While voters were hoping for the ‘reshoring’ of supply chains to the US, the likely effect is that large corporations will keep their current suppliers and pass on the price increases to the end customer within the US itself.

Trump’s policies could dampen US growth, and consequently global growth, but the jury is out, so watch this space.

Inflation: The never-ending story

Inflation has been hard to shake of late but 2025 looks somewhat more promising.

Towards the end of 2024, the developed world managed to shake off the sticky, high inflation that plagued markets since late 2022. In the UK, inflation eased throughout the year in response to aggressive rate hikes from the Bank of England (BoE), but inflation is still likely to tick upward into 2025.

The US told a similar story, with the Consumer Price Index (CPI) approaching the Fed’s 2% target while remaining persistently high. Emerging markets, meanwhile, have experienced both hyperinflation and deflationary risks across various regions.

Asset Class Returns

Markets enjoyed a relatively calm year overall, despite a volatility spike in August triggered by fears of a US recession and an interest rate hike at the Bank of Japan. This was a brief blip that passed quickly.

The positive story of the year was the long-awaited return of fixed income, as central banks began gradually reducing interest rates. This shift also contributed to the resurgence of emerging markets, as cheaper debt spurred growth in companies within these regions. The US continued to deliver strong returns, driving global growth.

Equities

Developed markets leading the charge

Markets were once again dominated by the so-called ‘Magnificent Seven’. They defied expectations to return a collective 44.2%, compared to the rest of the S&P 500, which returned just 27.6% as of 27 November 2024.

Source: Reuters & LSEG (2024)

The “Magnificent Seven” stocks are undeniably dominating the US equity market, and their growing share of market capitalisation has raised concerns about overconcentration. These firms are global giants with extensive operations worldwide and combined revenues that exceed Australia’s GDP. The scale of the Magnificent Seven’s financial footprint is immense.

Source: GDP data from the World Bank, revenue data from company financial statements and Macrotrends (2024)

Equity returns elsewhere in developed markets were solid. Japan had a recovery year after a long period of underperformance, but Europe struggled, returning just 4.60%. The UK had a positive year in the markets, with UK equities returning 10.02% over the year.

Resurgence in Emerging Markets

Emerging markets have faced significant headwinds in recent years, including high interest rates, political instability, and increased tariffs, causing them to lag behind their developed counterparts.

In 2024, performance was mixed, with periods of high returns eventually giving way to generally flat markets as the year ended. Developed markets delivered an impressive 21.2% return compared to emerging markets’ 9.33% for the year. While this may seem underwhelming, it marks a significant improvement from the 3.69% return achieved by emerging markets in 2023. Easing economic conditions could serve as a springboard for potential growth in the region throughout 2025.

Source: Timeline (2025)

Fixed Income

After several challenging years for the fixed-income asset class, bonds finally staged a recovery in 2024. While they didn’t achieve the high returns seen in equities, they delivered a respectable return of 3.32% for the year.

Central banks worldwide began the gradual process of lowering interest rates following the sharp hikes implemented during the Covid-19 pandemic. Notably, the UK and the US played significant roles in this trend, reducing their rates to 4.75% and 4.25% to 4.5%, respectively, by the end of 2024.

This trend wasn’t confined to developed markets, as a global pattern emerged of central banks reducing their policy rates throughout the year. The graph below highlights various countries and their respective terminal rates. For fixed-income investors, 2024 has been a strong signal that the tides are finally turning. With further rate cuts anticipated in the coming year, this narrative is likely to continue evolving.

Source: Investment Week (2024)

Portfolio Performance

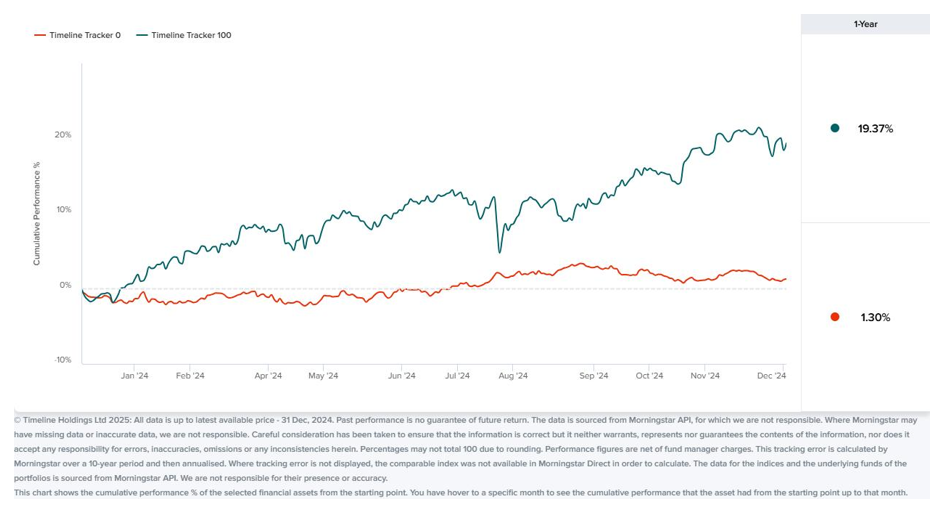

Timeline Tracker

This year has been a positive one for global markets, and this has been reflected in the performance of our Timeline Tracker over the period. When reviewing one-year returns, the equity portion of the portfolio, Tracker 100, has successfully achieved its goal of effectively capturing global market returns. With a return of 19.37%, it reflects the positive sentiment in the markets and the growing investor confidence heading into the new year.

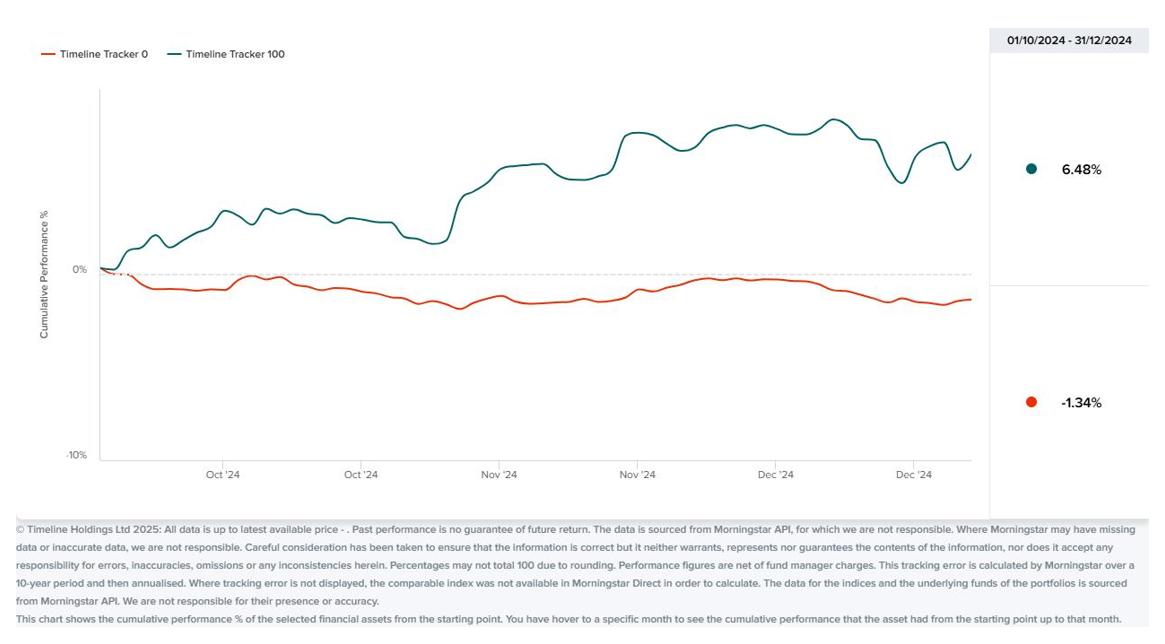

The fixed income portion has continued to provide steady returns on the defensive side of our portfolios, as measured by the Tracker 0 model. However, with inflation proving stickier than anticipated, central banks opted for a gradual, laddered approach to interest rate adjustments rather than making drastic changes. Despite this, fixed income performance dipped in the final quarter, closing December with returns of -1.34%.

With inflation currently hovering just above the 2% target in the UK and interest rates at 4.75%, there is optimism for fixed income in 2025 as conditions appear to stabilise and improve for the asset class.

Source: Timeline (2025)

Source: Timeline (2025)

Source: Timeline (2025)

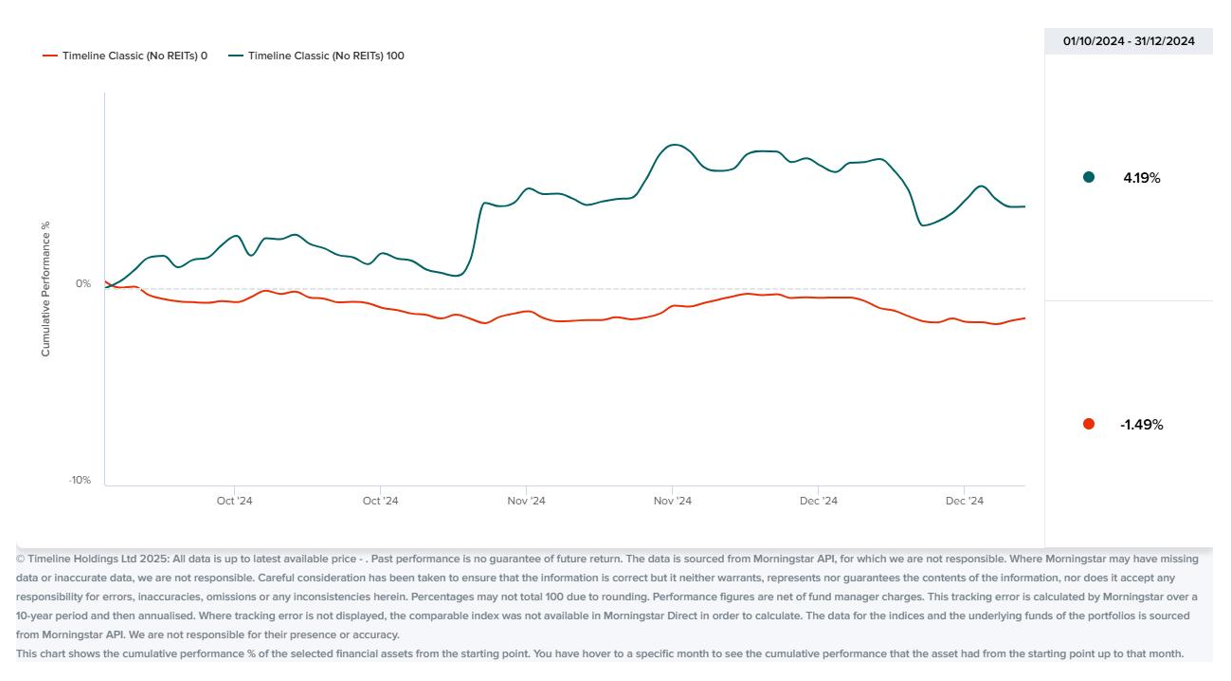

Timeline Classic

The Classic portfolios have performed well over the past 12 months in line with global markets. However, due to the range’s tilt towards small-cap, value, and emerging markets, they have slightly underperformed their Tracker counterparts. The Classic 100 model returned 14.94% over the past year. This slight underperformance compared to the Tracker range is primarily attributed to the strategy’s overweighting of risk premiums.

Value stocks have maintained solid performance over the past year, slightly trailing their growth counterparts. However, the small-cap and emerging markets sectors faced challenges, which contributed to the overall lag in the Classic portfolios’ performance.

On the fixed income side of the Classic range, over the year the 0 model returned a promising 1.14%. With the range’s tilt towards the slightly shorter maturity end of the spectrum, the reduction in interest rates has favoured bonds with a longer maturity. This had a knock-on effect, with the 0-model returning -1.49% over the last quarter.

Source: Timeline (2025)

Source: Timeline (2025)

Source: Timeline (2025)

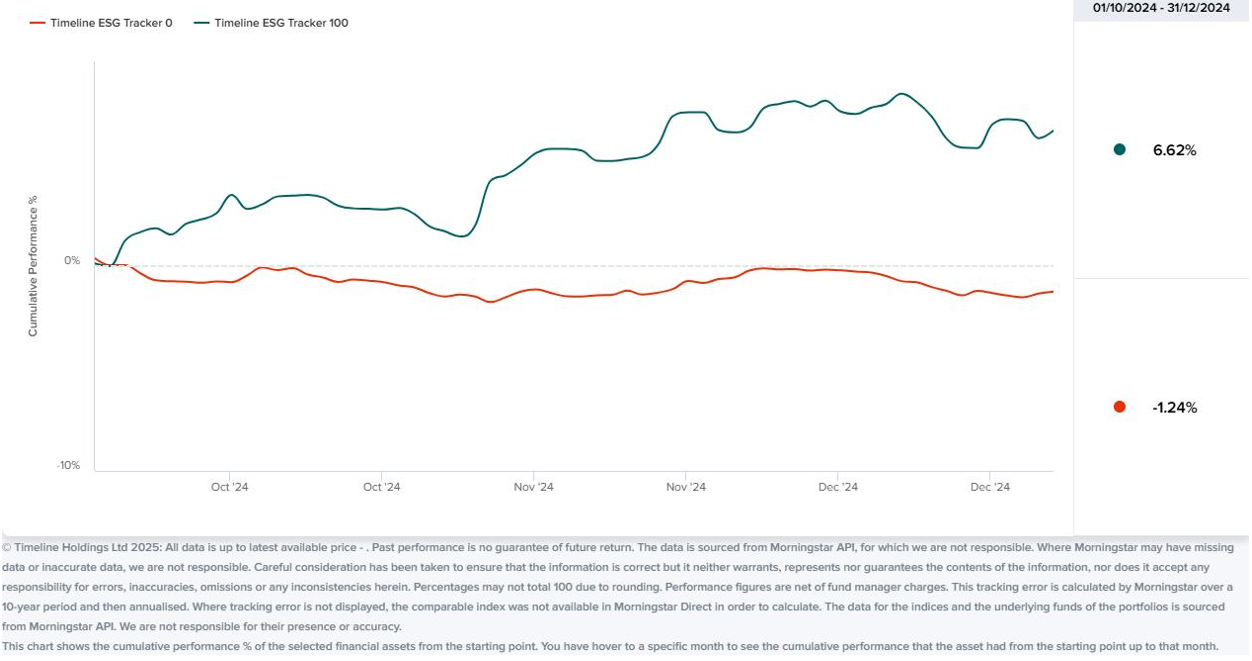

Timeline ESG Tracker

The ESG Tracker range benefited significantly from the positive market trends of 2024, much like its non-ESG counterpart. The ESG Tracker 100 delivered an impressive annual return of 20.11%, making it the highest-performing portfolio among our “core” ranges.

While maintaining global markets as its foundation, the ESG portfolios place additional emphasis on securities with higher ESG ratings and underweight those with lower scores on these ESG metrics. This strategic tilt, combined with another strong year for technology stocks, contributed to the portfolio’s exceptional performance, as the overweight to this sector proved particularly advantageous.

As with the broader Timeline Tracker range, the ESG Tracker’s fixed-income holdings closely mirrored the performance of the wider global markets. The defensive portion of the portfolio posted a 1.2% annual return, though performance in the final quarter detracted slightly from the overall result.

Source: Timeline (2025)

Source: Timeline (2025)

Source: Timeline (2025)

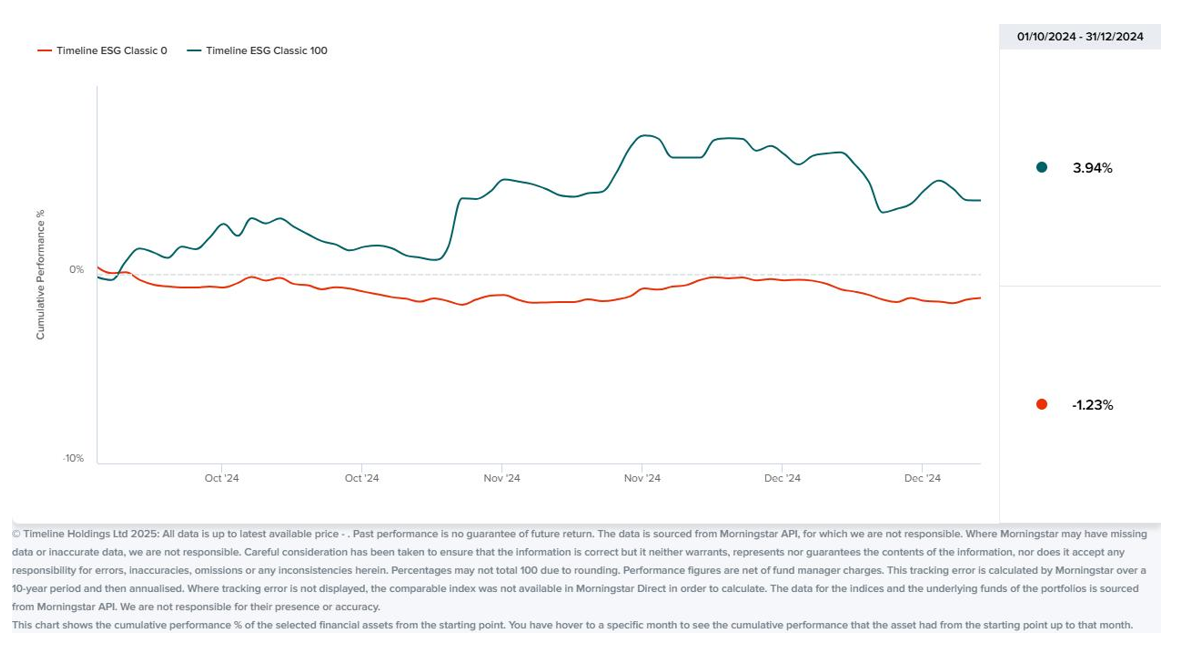

Timeline ESG Classic

The ESG Classic range delivered a 14.29% return for 2024, performing in line with the non-ESG Classic range.

Again, the portfolios overweighting to the small-cap portion of the market has caused a dampener on returns as the large-cap tech stocks have once again driven equity market performance in 2024.

The fixed income portion of the portfolio has mirrored the Classic range with a return of 1.35% for 2024. The ESG Classic 0 portfolio suffered, like the other core ranges, in the final quarter of the year, leading to a return of -1.23%.

Source: Timeline (2025)

Source: Timeline (2025)

Source: Timeline (2025)

Final Thoughts

While 2024 was a year filled with events destined for the history books, it proved to be a steady and relatively quiet year for markets. 2025 is truly an unknown playing field. Trump will begin settling into his old chair in the Oval Office and enacting some of the promises he made on the campaign trail. While not all of these pledges may materialise, their potential impact will be closely watched worldwide. On the global stage, calls for ceasefires and peace will continue as conflicts show little sign of resolution early in the year.

Finally, AI has been a buzzword in 2024, and it’s likely to continue this year with developments in technology and regulations around it.

The year ahead promises to be one filled with opportunities, excitement, and trepidation. Volatility will likely rear its head in 2025 and bring with it some movement in markets. Our philosophy remains steadfast: we don’t attempt to predict future market movements. Instead, we focus on helping you achieve your financial goals and staying invested.

Production

Production